TL/DR: If the currency isn’t scarce, everything else on the planet that humans desire will become scarce.

I’ve spent the last 15+ years (since the ’08 financial crisis) trying to figure out how to manage money during unprecedented times. We are living in an experiment. My guess is you are going to have to try new things (while also adhering to some old things) to thrive! I doubt I have it figured out, but I’m closer than I was. Here’s why I’m doing what I’m doing. I hope you find it helpful in thinking about your financial journey.

If you’d rather read this in a PDF it is here:

When Things Changed For Me

When the 2008 financial crisis hit, I was impacted (as many were). I’d been out of college for 13 years and this was the first time I’d lived through a financial crisis where I had some accumulated wealth on the line. By the time the stock market finished crashing in November, I’d lost 2/3rd of my net worth (on paper). Seeing some relatively large numbers drop down to be much smaller numbers was humbling (and very scary). I had made a series of stupid financial decisions leading up to the wheels coming off the global financial system. Regardless, I stuck with things throughout the crisis, and everything recovered in due time. This was probably as much luck as it was my own steel-belted temperament. It was not fun, however, at any point along the way. There were days it felt like life was gut-punching me. I realized during that time how fragile the entire economic system is (which my life is latched onto). As I survived this, I learned some hard lessons and made changes in my life that were permanent in nature. Life is too short to ever be that stressed out about money.

However, my net worth and investments bouncing around like a basketball was not the biggest problem I felt like I had. The RESPONSE to the 2008 financial crisis was deeply disturbing to me. Manipulated interest rates and manipulated money had both gone to absurd levels during the crisis. This was more disturbing to me than the crisis itself. It didn’t make any sense to me (and still doesn’t now).

Manipulated Interest Rates

Interest rates have been centrally planned for many years. You might believe this is good or bad. I know I have my opinions (but we’ll stick with the facts). In the early 2000s central planners got very aggressive with low rates (and eventually took us to the zero bound). We’d gone through the internet stock bubble in the 2000s and by 2008 a housing bubble was breaking the entire world economy (only a few short years later). The response from the Federal Reserve (the US central bank) to the 2000 crisis was to drop the Federal Reserve Effective Rate to 1.75% and then down to 1.00%. These were generational lows. In the leadup to the 2008 financial crisis, they stepped rates back up to 5.25%. This didn’t matter as ultralow rates had led to a brewing housing bubble. When the 2008 financial crisis hit they quickly lowered rates to basically 0%. In early 2016 they began raising them again and got to 2.4% before COVID hit and they were lowered to 0% again. For the past 14 years, we’ve had manipulated interest rates set at 0% and never above 2.4% (briefly for some of 2019). In a recent change of heart to ‘fight inflation’ the Federal Reserve has been jacking up rates aggressively (since 2022).

When rates were lowered after the 2000 crash it was disturbing. Who are these people and why do they get to decide what rates should be and how low they need to be? When they went to the zero bound after the 2008 crisis, I was angry. What in the hell are these people doing? I used to earn money from my savings now I guess I earn nothing because these people decided so. I remember thinking how stupid this policy was. The longer it played out the more absurd I believed it to be. How can an economy function if the cost of capital is zero?

If you believe that a group of humans can set the cost of capital (via interest rate policy) better than a free and open worldwide economy you are wrong. Full. Stop. I won’t even argue with anyone about this topic because the other side of that argument is completely asinine.

Manipulated Money – Part 1 – Central Bank Balance Sheets

The same thing happened with the money. A new program was created by the Central Banks called QE (Quantitative Easing). It has subsequently been called all kinds of different things but the effect remains the same (money printing and/or asset price support).

Global Central Banks almost doubled the size of their balance sheets during the 2008 financial crisis (with the US Federal Reserve leading the way). They went from $5 trillion to just under $10 trillion over the course of two years. Every new crisis along the way leads to more balance sheet expansion. By the time 2020/COVID (10-is years later) arrived they’d doubled things again to around $20 trillion. Within a few years after COVID, they’d blown past $30 trillion. If an asset was impaired the Central Banks would take the assets onto their balance sheet. No one ever loses money again. Come for capitalism’s gains, stay for the socialization of losses! Boom, problem solved!

Manipulated Money – Part 2 – Deficits

The last step of removing any real-world consequences from the fiat-based US Dollar system happened in 1971. In 1971 the US Dollar was no longer convertible to gold, and it became a completely paper-based fiat currency. The US Dollar now floats against all other country’s fiat-based currencies. Being the global reserve currency has allowed the US to run deficits for many decades. The US has taken full advantage of this ‘exorbitant privilege’ fully during that time. In recent years we’ve run trillion-dollar deficits regularly (even $3 trillion in a single year during the COVID crisis).

We are currently on track to spend $6 trillion in the current year while revenue is going to be around $4.6 trillion for a deficit of $1.4 trillion. Politicians, you’re doing great!

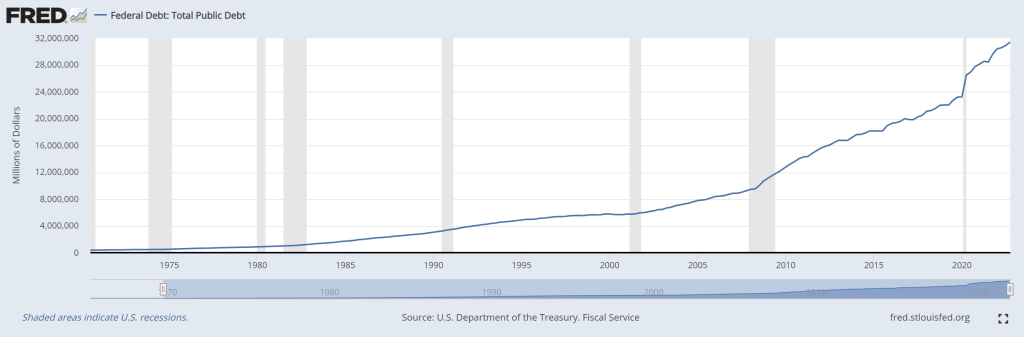

Manipulated Money – Part 3 – US Debt

All those deficits add up and become the US Debt. This currently stands at almost 32 trillion dollars (or 120% of GDP). We are currently on track to pay $928 billion in interest in Q1 of 2023. Remember, rates are rising fast, so this amount is rising fast (it was only $600 billion a year ago).

These US Debt numbers do not even count the ‘off balance sheet’ items that are linked to enormous entitlement programs that have future outlays tied to them (for Social Security and Medicare). The total amount outstanding for those entitlements is about $187 trillion at this time. But don’t worry this money is held in a ‘trust fund’. This means that the government took this money from your paycheck and immediately spent it in that year’s budget. So that money is gone! But don’t worry it put an IOU into a ‘trust fund’. This means that it owes that money back to you when it is due. So, we’ll need to come up with another $187 trillion to do that. See, everything is fine! Not! Utter insanity!

Manipulated Money + Manipulated Interest Rates = Manipulated Cost Of Capital

As time has passed I’ve come to realize that the manipulated interest rates and manipulated money were manipulating the cost of capital. A few people in a room along with our government were 1) setting interest rates artificially, 2) creating money artificially. These two things set the cost of capital for everything else on earth.

Every asset on earth derives its valuation based on the cost of capital (i.e. interest rates and available money supply). If interest rates are low and expected to remain low (or go lower) the price of an asset should remain elevated (and vice versa). If more money is available to chase an asset then the price of the asset should remain elevated. Supply meets Demand!

Interest rates have been pegged (artificially or manipulated) at zero for over a decade. Global Central Banks currently have $30 trillion of liquidity via their balance sheets injected into the financial system. Additionally, the US Government has spent $32 trillion of money that didn’t exist (via deficit spending) into the economy over the past few decades.

What does $62 trillion injected into the financial system do to things like stock prices? That enormous total at near-zero interest rates pumping liquidity provides a lot of support to the US stock market. The US stock market is only valued at around $45 trillion and the total global stock market is valued at around $90 trillion. $62 trillion will make a dent (to the upside) for sure!

Everything on this table (which is pretty much everything investable on earth) benefits from low rates and available money when the cost of capital is low (even if it is artificially low or, gasp, manipulated).

What this means is that if you did not borrow money (cheaply) and buy risk assets you were an idiot. Sorry, the truth hurts! Money was basically free and risk assets were not. All the bidding/buying boosted risk asset values. All the smartest FinTwit people knew this and bought risk assets hand over fist. They looked down upon the ‘more stupid people’ who were not as smart as they are. The smarty pants FinTwits would openly mock people on Twitter if they tried to point out how the system they were operating within was manipulated (and unsustainable). They had little self-awareness about the great benefits bestowed upon them by the Cantillon Effect. Perhaps a better approach would have been to shut their mouth and accept the gift bestowed upon them quietly. Instead, they would point to how wise they were and how dumb everyone else was. Indeed they were smart. They’d identified the rigged game and were playing it well. Don’t hate the player, hate the game. I do hate the game (and I’m not too fond of many of the players either)! Anyone using common sense and not buying into the scheme/scam has been punished for their level-headedness.

What all of this means is EVERYTHING IS MONETIZED! Every asset is bid up and overbought because the underlying cost of capital is broken. Let’s look at some examples of some of the largest asset classes.

Monetized Asset – Stocks ($SPY Performance Since 2008 461%)

Worldwide stocks account for about $90 trillion in value. The US stock market accounts for about half of that and has been one of the best-performing markets on earth since the 2008 financial crisis (minus India) with a 461% return since the 2008 low. If you bought and held stocks since the 2008 financial crisis you have been rewarded.

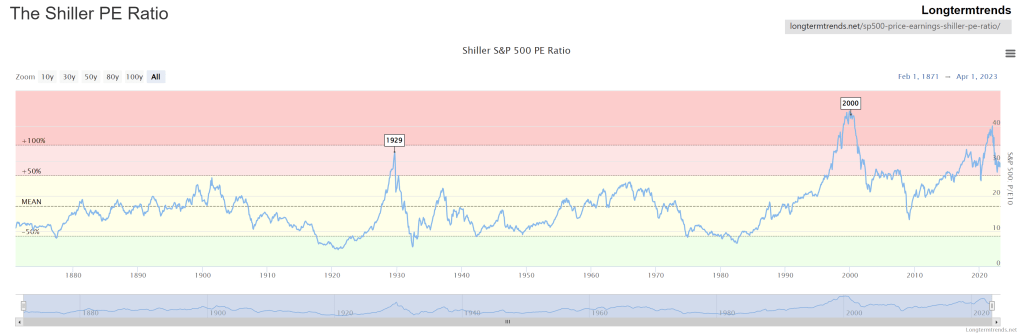

For this to happen companies had to 1) stay in business, 2) operate and grow and 3) do everything companies normally do. But really all they had to do was simply 1) exist and 2) ride a wave of multiple expansion. The Shiller PE Ratio shows the multiple expansion (or contraction) using the rolling 10-year earnings history of the company. As you can see from this chart the price multiple on the S&P 500 has expanded greatly since the 2008 financial crisis bottom. It is currently at the 4th highest level it has ever been in history (since the late 1800s) and is just off the second-highest value of all time. Stocks are up and the biggest contributor to their return is multiple expansion. In short, this means that people are willing to pay more for a dollar of earnings than at almost all times throughout history. Manipulated money has driven people to stuff money hand over fist into stocks searching for any type of return (since they can hardly earn anything sitting on cash).

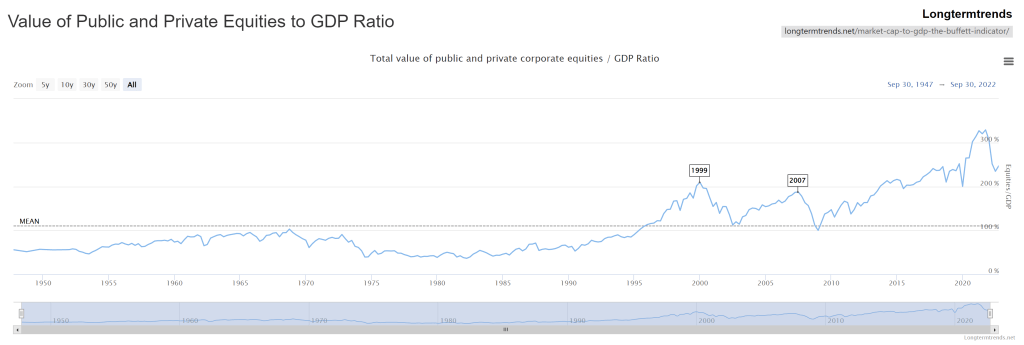

If you pull out a Shiller PE ratio chart with anyone on FinTwit you’ll be stigmatized, greatly. You’ll be told how you don’t understand the new paradigms of valuation and blah, blah, blah. So, another way to easily see how monetized US Stocks are is to compare their value to GDP. Again, even after a big decline from the recent peak valuation, we are still at an unprecedented level.

Either way, you look at it people are driving the value of stocks up via multiple expansion. The monetization of stocks from the manipulated cost of capital is apparent. The problem with this scenario is you are damned if you do, and damned if you don’t. If you buy stocks and hold them when they are historically overvalued you had best be prepared to hold them if conditions change (and they get much cheaper). If you do not hold stocks because they are historically overvalued you are being left behind as they rise and presumably you sit in bonds/cash earning almost nothing (while also being ravaged by inflation). Only recently have cash savings begun to pay anything and change this equation.

When the cost of capital is manipulated the ability to use logic and reason are removed from the equation. You are just along for the ride (and it will probably be a wild one). Good luck, and thank your central planner for the opportunity!

Monetized Asset – Real Estate ($VNQ Performance Since 2008 243%)

Real estate is the largest asset class on the planet. It accounts for about $281 trillion in value. There are plenty of ways to gain access to real estate (actively and passively) and to the different kinds of real estate (commercial, residential). Buying the largest REIT ETF is one way. The real estate market has been the second best-performing market on earth since the 2008 financial crisis with a 243% return since the 2008 low. Even with a housing collapse if you had bought and held real estate since the 2008 financial crisis you have been rewarded.

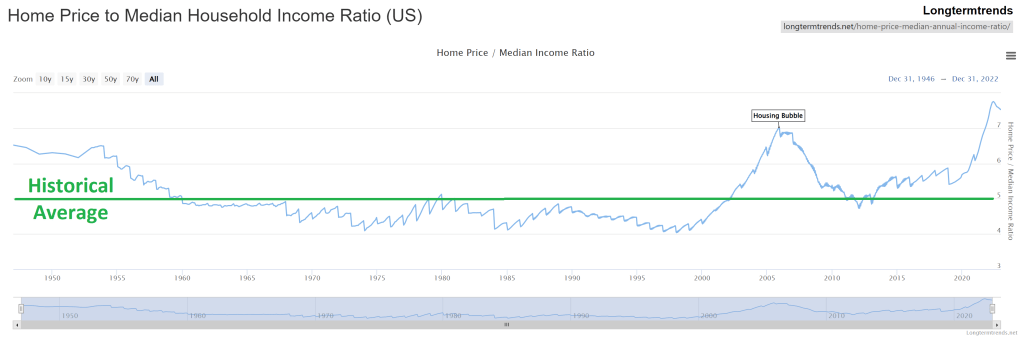

But, if you look at home prices in the US you’ll see a similar monetization problem. The real estate is the same as it was (no new revelations in dirt and buildings have been invented). But the price people are willing to pay for it has skyrocketed. If you compare the median home price in America to household income you’ll see people are committing more and more of their household income to make the purchase. It was recently even higher than during the housing bubble. You know, the one that started the 2008 financial crisis. The median house price was $208k at the bottom of the housing crash in 2008 and recently topped out at $479k (in Q2 2022).

When the cost of capital is manipulated the ability to purchase a home to live in evidently becomes extremely hard. You face a lot of competition. You are competing against other people looking for homes to live in. You are also competing against big institutional investors who are looking to park money in an asset that will provide them with a return. It seems even the largest asset class on earth is not immune to being monetized when the cost of capital is manipulated. Find a bridge to live under and thank your central planner for the opportunity!

Monetized Asset – Commodities ($GLD Performance Since 2008 129%)

Commodities are a tough investment class to nail down. It is a good asset class to look at since it is tethered to the real world in a way other asset classes might not be. The largest weightings are energy, agriculture, precious metals, industrial metals, and livestock. These are all real-world items we use daily to survive. It is very difficult to buy/own a commodity position unless you have a place to physically store all of it and a way to buy/sell it. Some ETFs provide exposure to the asset class (via futures markets) but they are not ideal in many ways. For simplicity, I took the largest gold ETF (which has been around since the 2008 financial crisis) to get a sense of how commodities have done since that time. Gold is around a $11 trillion asset class and is a reserve asset for many institutions throughout history. The gold market has been the third best-performing market on earth since the 2008 financial crisis with a 129% return since the 2008 low.

Commodities tend to 1) move in long cycles of inflation and deflation and 2) can move wildly when they move (an extremely volatile asset class). In the years leading up to the 2008 financial crisis, they had been going gangbusters. Since 2008 as financial markets have performed well they have underperformed. Why own anything ‘real’ when you can just buy stocks and watch the money grow through the effects of monetization? Commodities have had a few stellar years recently. It remains to be seen if that is related to post-COVID supply chain restart issues or if a new commodity cycle has started.

One truth in the commodities asset class is that commodities get cheaper over time. With technology gains, we can produce more with less. NOTE: This is a very important point that one needs to understand. Technology and human ingenuity make EVERYTHING cheaper over time. More on that later!

Since commodities are less related to the manipulated cost of capital and are more tethered to the physical world, they are in theory less monetized than other asset classes. This is likely not the case, however, since commodity producers rely on the manipulated cost of capital to develop production. Why would producers invest their capital in expensive projects to do all that hard, risky work when they can just invest the same capital into financialized investment products and earn more (with a lot less work/risk)? Admit it, that is what you’d do! Lazy! Commodity producers are just like you, they don’t jump out of bed every morning dying to work like a dog all day for little gain. If they don’t see a potential return for their work, they’ll skip it!

Monetized Asset – Inflation (CPI Performance Since 2008 43%)

You don’t invest in ‘inflation’ but everything you do with investing and savings is to beat inflation. So, it is extremely important to understand how it plays into one’s investment portfolio (and spending).

Inflation is a wrecking ball that destroys wealth. It doesn’t care about your wealth, your income, or anything else. When it is rolling along at 2-ish% a year no one seems to care too much (I do, however). Regardless, it will take many years to wipe out your wealth. When it kicks up to levels we’ve seen recently (7-ish+%), it is a wrecking ball that can quickly change your wealth equation.

So, if you had $1.00 at the end of the 2008 financial crisis you’d now need $1.43 to have the same amount of spending power…THROUGH THE POWER OF INFLATION! This seems like a great system!

This is straight off the US BLS website. If you believe their CPI index is an accurate measure of actual inflation, I feel sorry for you. NGMI! The government that is debasing your currency should not be trusted to tell you how much they are debasing your currency!

There are many other ways to determine inflation and it is different for everyone. Your personal inflation rate is how fast the price of whatever you are spending your money on is going up.

I have many thoughts on inflation and how evil (and unnecessary) it is. Remember when I talked about how technology and human innovation make everything cheaper over time? That is true. If we didn’t have a monetary system that is designed to debase (via inflation) our lives would continue to get easier and cheaper with each passing day.

That doesn’t feel like what is happening in the world I’m existing in these days. It doesn’t exist in the world that the US government tells you exist today (using their own CPI index). That world shows that you need to earn more and more to keep pace with the rising costs of everything. If you want to save and beat inflation you better be well ahead of the pace the currency is being debased (which in this period was 43%). For this, you can squarely thank your central planner for the opportunity to constantly fight the laws of technology and human ingenuity. Work harder, peasant!

Monetized Asset – Bonds ($TLT Performance Since 2008 1%)

“Why would anyone own a bond?!?” – Deano

Bonds account for about $253 trillion in value. The bond market has been one of the worst-performing markets on earth since the 2008 financial crisis with a 1% return since the 2008 low. If you bought and held a bond ETF since the 2008 financial crisis you have NOT done well. BUT WAIT, THERE’S MORE!

You’ve earned extremely low yields due to manipulated interest rates and quantitative easing. Your bond investments are competing with people that can print money from thin air and set rates to whatever they want them to be. How can you win? PS – You can’t/won’t!

You’ve also been on a wild ride along the way as rates were hitting lifetime lows in 2020 but have risen sharply in recent years wiping trillions of stored wealth off the map. Bond investors have grown complacent over the past few decades as lower and lower rates made them wealthy (with very little risk). But when we hit the zero bound things got weird and the outlook isn’t good.

With inflation debasing your wealth (and recently at a rapid clip) and bond investors earning nothing in the process, their wealth is being destroyed.

- Since the 2008 Financial Crisis – We just reviewed how inflation has turned $1.00 into needing $1.43 today (-43%?). Now we see how bonds during the same period have returned 1%. Bond investors, with their money invested in a ‘safe asset’ backed by the full faith and credit of the US Government, have lost 42% of their purchasing power in 15 years (as prices continue to rise while their wealth does not).

- The Past Two Years – In the shorter term, over the past two years, we’ve had back-to-back high inflation (7.04% in 2021 and 6.45% in 2022). If inflation is making the price of everything you want to buy go up 14-ish% over the past two years and your stocks and bond portfolio is down 13-19% (like it was in 2022) then you just got 27-32% POORER in a very short amount of time. PS – THAT JUST HAPPENED TO YOU!!!

By the way, for all the people who say inflation is coming down so everything is fine. YoY we just had 4.93% inflation reported for April. Awesome, that is lower than it has been. BUT…Inflation compounds! That 4.93% is on top of the prior YoY value in April 2022 of 8.26%. We aren’t out of the woods yet!

I often say “Why would anyone own a bond?” What I just described is why I say that. The world is awash in cheap debt that will NEVER BE PAID BACK! [“like ever” – Taylor Swift]. It can’t be paid back or the entire system collapses. A debt-backed system can’t deflate the debt without collapsing the values of the assets within the system. As we’ve covered, all asset prices are monetized by low rates and extra liquidity. If interest rates rise dramatically and/or the debt-backed balance sheets are reduced (QT) then all of a sudden asset prices will no longer be monetized (i.e.asset prices will fall). We can’t collapse the value of the assets in the system without destroying the entire system. The value of those assets sits on balance sheets throughout the system and is the collateral for all the loans, are the thing driving the GDP/economy, and are responsible for paying the majority of the taxes, etc. If asset prices start collapsing, it will set off a chain reaction that will begin to spiral the debt-backed economy into a very dark place.

Rates can’t rise substantially and stay there because the interest to service the debt will be too much of a drag on the system. So, more and more debt with lower and lower interest rates will continue forever. All manipulated (via central planning) every step of the way!

The Central Bankers will act like they are worried about inflation but they only care about inflation if it gets too high and undermines their credibility (like it did in the past couple of years). They really don’t care if inflation is high (because it helps them by inflating away their debt more quickly). Deflating their debt away via inflation (and currency debasement) is their TRUE goal. I know they blab on constantly about employment and stable prices being their goal, but that is a sideshow. All they truly care about is NO DEFLATION (more on that in a moment).

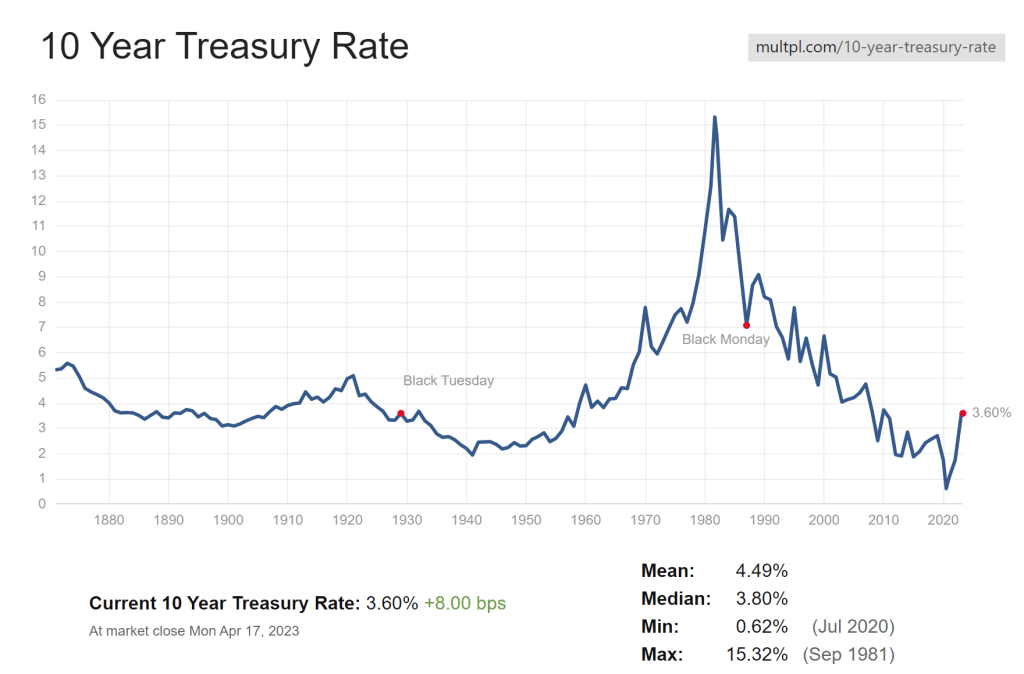

When inflation rises sharply and quickly they will put on a show and act like they are “fighting it” by trying to keep it around their 2% target. Even 2% is bad for you when your bonds are barely yielding that. If the inflation rate was 4.93% in April and your 10 Year Treasury is earning 3.6% (which it is) you do the math and figure out how poor you just got this year. Do it year after year and see what happens. Your purchasing power is being wiped away slowly over time in the best-case scenario where they hit their target 2% inflation. It is being wiped out much more quickly if inflation gets high. Either way, I promise you, the Central Bankers do not care at all!

The Central Bankers are REALLY worried about deflation. If that rears its head, then their entire system is at risk. If asset valuations begin falling and debt issuance stops (or even slows down greatly) things start to unwind quickly. This is why when it happens you see them start manipulating interest rates and the money supply quickly. They cannot under any circumstance allow deflation to exist.

Again, I’ll point the reader back to when I pointed out how technology and human ingenuity make EVERYTHING cheaper over time. You can see how the two systems are in direct contradiction with one another. You should be winning but you are losing because of the fiat-based, debt-backed system we are operating within.

THE DEBT WILL NEVER BE PAID OFF! IT CAN’T BE!

The debt is what is monetizing the entire system. Deflating the debt will collapse the system. So, you can’t unwind the debt, you can only continue to grow it. Even if the growth rate slows down it threatens the system. If we have $235 trillion in debt and it cannot ever be reduced or even slowed down without collapsing the entire system, you can see the predicament we are in. The debt must continually grow!

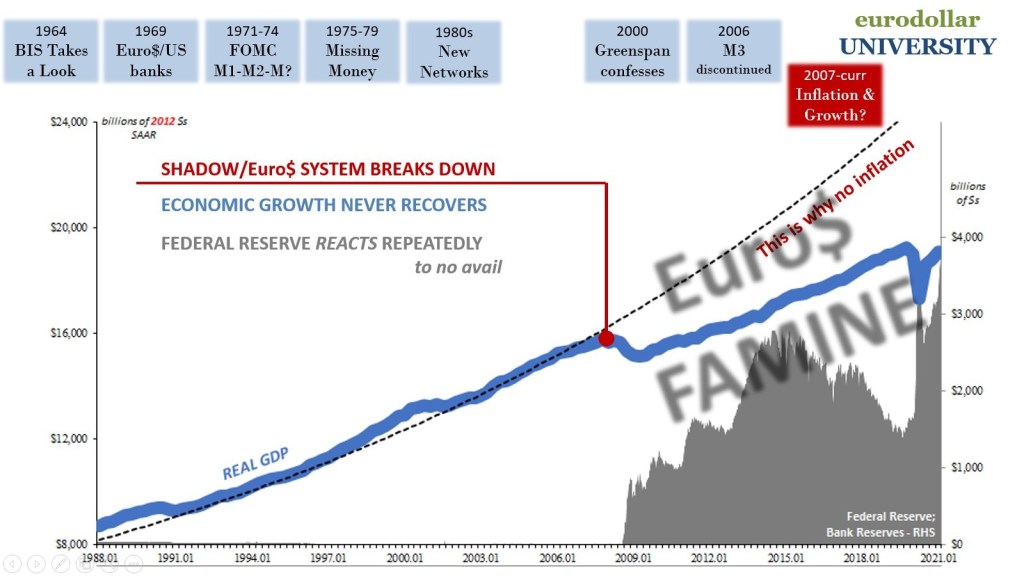

Since the 2008 financial crisis, the massive Eurodollar system has simply slowed the rate of debt growth down and it has had all kinds of negative impacts on the overall financial system. Forget decreasing the debt, just slowing its growth is causing major issues.

The Central Bankers have tried to assure everyone that everything is fine by manipulating rates and money printing (via QE), but it is a drop in the bucket compared to the entire debt market. If things slow down further the Central Banks will take on more and more of the system’s debt onto their balance sheet. To see how things play out look at Japan’s Central Bank which now owns the majority of the Japanese debt market. This will happen everywhere.

My guess is the dollar amounts in QE we’ll see in future ‘crises’ will be bigger and bigger and the total debt amounts will continue to grow larger and larger. The clown world of manipulation we live in will grow more preposterous each step of the way. The rich will benefit and the wealth gap will continue to grow wider and wider.

This is not investment advice but if you can find a way to borrow fiat-based paper money (that they are creating out of thin air) at a low rate to buy a real-world, physically constrained asset as an investment you’d be silly not to. They will make money for nothing but you can’t make real assets for nothing. One is tethered to ‘faith and credit’ and the other is tethered to ‘reality’. The hot-shot, brainiac FinTwit crew will approve of this plan.

Everything Is Monetized!

Everything I have covered has outlined why I was so disturbed by the response in 2008 to the financial crisis.

- I knew a few people in a room setting interest rate policy and rates to near zero was not a wise course of action.

- I knew that printing money from thin air, in the form of Quantitative Easing, and dispersing it into the investment landscape by a few people in a room was not a wise course of action.

- I knew that having a monetary system that is being run to debase the population’s wealth by 2% (targeted) a year is asinine. Why on earth do we need that?!? But here we are!

- I started to realize that both of these things were manipulating the cost of capital which impacted the price of every single thing on earth.

- I started to realize that asset values were being propped up and even bid higher by both of these actions and that this was creating fake paper wealth that was unlinked from long-standing valuation multiples. Everything Is Monetized!

- I now realize that regardless of the unhinging from reality in risk asset prices I had to own them anyway. Otherwise, I’d be left behind and my wealth would be ravaged by the impacts of inflation. Buy and hold on for dear life! It won’t be fun!

Over the years, I have struggled with all this greatly and how to structure my investment portfolio to handle it all. Frankly, I knew the way to do it but it was unsettling and did not leave me with any confidence. I was working within a system that was rigged (and manipulated against me). That isn’t what you want when you are dealing with your entire life’s wealth. The existing fiat-based, debt-backed system forces us to contemplate all this on the daily, however. If you are not contemplating it and fighting it you will lose wealth (i.e.your life force). We can’t just work hard, save money for the future, live and die. We are forced onto a treadmill that forces us to earn more and more for longer and longer to thrive (or even survive). Life gets harder every day instead of us being allowed to reap the rewards of technological innovation and human ingenuity for our life to get easier. I have more wealth than I have EVER had, yet I feel no more peace about it due to the fragile and highly manipulated system it is contained within.

It’s Worse Than You Think!

Worst of all, after all this wild gyration it doesn’t even matter! What?!?

Deano, my stocks are up huge since 2008 and my house is worth twice as much as it was then. I’m rich! – Everyone

You keep telling yourself that. As I said before, I have as much wealth as I’ve ever had, but I don’t feel rich! Why?

Preston Pysh went down this rabbit hole in a Twitter thread back in late 2021/early 2022. He figured out that despite the large returns of stocks that if you account for the currency fluctuations and the growth in the M2 money supply you were only up 7% from the bottom in stocks in 2009 through the end of 2021. 12 years and you only made a measly 7% due to debasement. Not quite the 461% that I presented earlier in this paper. By the way, the stock market is down 14% since Preston did his analysis. But so is M2 (but not that much). The government did change the way they calc M2 in late 2020 (surely not for any nefarious reason…we trust them…right?!?). This is a very interesting thought experiment. The link to the thread is here (https://twitter.com/PrestonPysh/status/1470792736626331659?s=20).

So, everything is monetized and based on a manipulated cost of capital. Interest rates are manipulated. Money is printed from thin air. Asset prices are bid to the moon. And a debasing currency might be eating up every dollar of gain we think we are making. Great! What is one to do?!?

Enter Bitcoin! Somewhere along the way in my 15-year investing journey, I learned about Bitcoin. I studied it for a few years (first started learning about it in mid-2017). Then after a few years (and a few hundred hours) of learning, I finally bought some (in late 2019). Since then, I’ve studied it a ton more and have increased my allocation to it over time.

Bitcoin is a COMPLETELY DIFFERENT system from the fiat-based, debt-backed system described so far. It is also completely outside that system. That is vitally important, IMHO!

Bitcoin ($BTC Performance Since 2008 6,000%+)

To me, Bitcoin has properties that allow for an escape from the fiat-based, debt-backed system that seems to be ready to topple or spiral out of control at any time. It seems to solve problems that allow for a different way to go about our existence.

“Deano are you really going to try to tell me about your magic, made up, internet money again?!?” – Everyone

Yes! Bitcoin was created and unleashed into the world during the fallout of the 2008 Financial Crisis. Evidently, I wasn’t the only one extremely worried about the response to the financial crisis.

We know Satoshi was worried about the response because of this:

The first ever Bitcoin block, known as the Genesis block, also contained a message. This was, “The Times 03/Jan/2009 Chancellor on brink of second bailout for banks.” Satoshi Nakamoto, the pseudonymous inventor of Bitcoin, included this message from a Times newspaper article on the day the block was produced.

Luckily Satoshi was a bunch smarter than I was and figured out the double spend problem, difficulty adjustment, hashing, stock-to-flow, and the 21 million supply issuance cap that birthed a brand-new asset class into the world. Bitcoin is perfect money. The world’s first perfectly decentralized and auditable money!

I could go on and on about those last two sentences, but others have done far better than I’d ever be able to do. In short, Bitcoin is better money because of: divisibility (not divisible), durability (doesn’t decompose), recognizability (fully recognizable), portability (completely mobile), scarcity (predictably scarce).

If you want to better understand why Bitcoin is different (and better) than any other money we’ve ever seen give Robert Breedlove’s What Is Money podcast a listen. If you want to understand why Bitcoin is THE apex asset and apex money listen to his Saylor Series with Michael Saylor. If you want to understand why Bitcoin’s Proof of Work model is part of its unique power listen to his Lowery Series with Jason Lowery.

Real World Constraints

The first thing anyone I talk to about Bitcoin says is it is made up and also printed from thin air. Technically, yes it was created by Satoshi and created from nothing but math and code. He then gathered up some processing power and spent money to buy some real-world energy to mine the initial coins that might have never been worth anything. He expended time, money, and energy (all real-world constraints) to develop something that he hoped would have value at some point. He developed Proof of Work!

By the way, this process continues today. Bitcoin miners have massive data centers and dedicated, specialized mining rigs that consume a lot of energy to mine new Bitcoin and subsequently store digital energy. They do this for the same reason that Satoshi did back in 2009.

People who talk about ‘changing the code’ to a Proof of Stake system away from the current high energy usage Proof of Work system do not understand how Bitcoin works at all. If we convert to a Proof of Stake model we will simply recreate the system we have today where a few people control the system with no real-world costs associated with their manipulation. The ENTIRE POINT OF Bitcoin is to be decentralized and to incur a real-world physical cost of time/energy to operate the system. Moving to Proof of Stake would indeed make it “magic, made up, internet money”?!? Hard pass! Proof of Stakers are NGMI!

The only way to get any of the 21 million Bitcoin that will ever be created is to 1) expend real-world energy to mine it (by the way about every 4 years this new supply miner reward gets cut in half) or 2) trade “real-world money” for it to buy it from someone else who already owns it.

So, Bitcoin is an energy-backed asset. If people believe it has value they will hold onto it. If more and more people believe it has value they will buy it from the existing supply/holders and the price will rise. In my opinion, it is not printed from thin air but is tied explicitly to the costs of energy in the real world. If you want it you have to expend real-world energy or capital to create it, transfer it, attack it, etc.

This real-world, energy-based constraint is THE reason it is different from the fiat-based, debt-backed system we operate within today. A few people in a room can create new money, create new debt, and set interest rates without any real-world, physical constraint. No one can do that with Bitcoin.

When you compare the two systems they are not even in the same universe of reality. I believe that one is tethered to reality which makes it superior to the other (that is tethered to the whims of a few people).

Decentralized System

That brings me to my next reason why Bitcoin is important. No one is in charge of it, but all of us are in charge of it. The Bitcoin protocol is controlled by the miners and the nodes. Anyone on Earth can run a node (and a few hundred thousand people currently do). The miners solve the puzzle to mine the next block of transactions and send it out to the nodes who compare the puzzle’s solution to the answer set to make sure it is valid. When enough nodes give it the all-clear the new block is added to the Bitcoin blockchain where it will remain for all time. The decentralized node runners (which can be anyone within the system) enforce the rules. The only way to change the rules is to get all of them to agree to change the rules. To get them to do that you have to make them believe that the change benefits their Bitcoin in some way (increased value, security, etc). Everyone is motivated by keeping the system intact and operating because their value is tied up in that system. It is completely decentralized (no one can shut it down), very attack resistant (and grows more and more so the larger it becomes), and operates on rules that are available for every participant to audit at any time (open-source).

Compare that to the fiat-based, debt-backed system we have today.

- Centralized – It is completely centralized in every way. You and I have no power to impact the rules. Sure, you can vote for a different politician to carry out your wishes. But the people controlling the levers of the system are not elected. So good luck. “It’s a big club and you ain’t in it!” – George Carlin

- Attack Resistant – There is no way to attack the system or even take back control for yourself if you don’t like it. You are at the whim of the system. If they want you to be debased at 2% a year forever that is what you have done to you. The best you can do is operate within the system and hope to stay ahead of everyone else. The incentive becomes to become corrupt to stay ahead of others. Kleptocracy! What a great system!

- Rules Are Unknown / Constantly Changing – No one knows what the rules are (or will be). We rely on some figureheads to tell us what the rules (they came up with) are today. But, the people running it can’t even tell you how much money there is. The Eurodollar system is an offshore entity that no one controls, and that can create and destroy money at will (at their discretion). Not a single person on earth can even tell you how much money they control or even who they are. WHAT?!? The Central Bankers get on television and talk like they are in control, but it is nothing but a façade. They are responsible for massive sums of money within the system, and they are playing tiddlywinks in the grand scheme of things of a $253 trillion debt-backed system. The ever-expanding fiat-based, debt-backed system is spiraling out of control and NO ONE is in charge.

Bitcoin is so decentralized in fact that I often think of myself not as a citizen of any particular country at this point but a citizen of Bitcoin. It is the system I trust to store my wealth (i.e.life force). So, the other people within that system are my fellow citizens. I’ve met and listened to many of these people, and I trust them A LOT more than the ones I meet and listen to from the existing system. I’ve honestly never come across a Bitcoiner that I didn’t like or trust. Can you say the same about your favorite politician?

Manipulated Via Centralization

This current fiat-based, debt-backed system is operated by a few people who make all the rules and can change them as they see fit at any time. I’d argue we operate in a Kleptocracy today within that system. We are presented with news daily about corruption within our system. Greedy people from all walks of life doing things that are illegal, immoral, unethical, and unloving. Bless their hearts (or lack of one)! There are bad actors all over the place that add no value to humanity other than to increase costs for the rest of us (to pay for their crimes). I’m not just a conspiracy theorist, either. Okay, I am, but, there are people with bad intentions out there. Many of these people are in positions of power and use that power to take more while doing less. These sociopaths (or more likely psychopaths) serve us no use at all. In a kleptocracy, corrupt politicians enrich themselves secretly outside the rule of law, through kickbacks, bribes, and special favors from lobbyists and corporations, or they simply direct state funds to themselves and their associates. I believe we live in a kleptocracy. There are some good people in our government, but they are outweighed (greatly) by those with special interests and self-interest. Sad, but true. So, in the existing system, the best case is we live in a system run by honest people that is highly manipulated and designed to make you poorer over time (via inflation and a manipulated cost of capital). Worst case we live in the same system but it is run by evil, sociopaths/psychopaths. Either way, if this is the system that I rely on to store my wealth I’ll gladly opt out of that system completely. Why would I trust my wealth to it when a better alternative exists?

Keynesian Versus Austrian

I guess the biggest debate about money and investing these days is which is right: the Keynesian or the Austrian system.

Keynesians believe in more centralized (i.e. government) control of money and economics (i.e. central planning). They generally believe a floating fiat-based money supply isn’t an issue as it allows the economy to expand and contract as needed. We live in a Keynesian system (controlled by the elusive Eurodollar).

Austrians believe that money should be decentralized from governments and of fixed supply which will lead to deflation over time for those who work and store their wealth in money. Bitcoin is an example of hard money that could form the digital collateral for a system of this nature to operate effectively in today’s world.

Bitcoin is an incredible revolution that allows the Austrians their best chance to bring their ideology to life. I’ve listened to hundreds and hundreds of hours of podcasts on the topic over many years. I think the world (not the US necessarily) needs an innovation like Bitcoin. Our system is broken for sure, but I think its adoption will be driven by the people most hurt by the current system, the global unbanked (there are billions of them). There are billions of people on the planet that have no way to store their wealth. They are unbanked and/or live in a country with repressive monetary systems or political systems. They have no currency to store their wealth. They have no way to protect their property to store their wealth. But they do have a mobile device. Enter Bitcoin and the Lightning Network. With these tools (and maybe some stablecoins added into the mix) these people can transact with one another and store wealth in whatever regime they live. They don’t need a bank account and can skip the broken financial system completely. For this reason, I believe Bitcoin adoption will be driven by these people. Those of us living in the Western World can’t possibly understand the issues these people face or the help a system like Bitcoin can provide. Additionally, the US Dollar/Eurodollar system does not help these people in the slightest way. Alex Gladstein has done a lot of work detailing the way the monetary system (facilitated by the IMF/World Bank) is essentially global colonialism and not beneficial for anyone other than us. The Western World keeps our prices low by taking resources and labor from these developing nations (destroying their economies and livelihoods in the process). Bitcoin may also allow countries like these to remove themselves from these broken systems (see El Salvador). More power to these people!

Meanwhile, the Keynesians are doing themselves no favors by never taking away the ‘punch bowl’ that has allowed our finances to become such a mess. The environment since the 2008 financial crisis highlighted much of that insanity perfectly. We’ve had manipulated money (money printing and artificially low rates) set by government central planners for decades. I’m not sure a few people in a room can do a better job of managing the global economy than the global economy can do itself.

People on both sides of the debate discuss all kinds of wild theories: Deflationary Black Holes, Debt Spirals, Hyperbitcoinization, Reemergence Of Gold Back Currencies, Dollar Milkshake Theories, The Death Of The US Dollar As The Global Reserve Currency, CBDCs, etc. They are always in bold letters and said with lots of fanfare. I see their point most of the time. Regardless, I’m not sure I believe anything drastic will happen. I believe things will move along at a much slower pace but over time we do make a transition to a different/better system. If Bitcoin is that system I expect to see adoption increase and the Bitcoin price increase over time (but with big moves up and down along the way). I hope that it happens this way for all of our sake. If we get some kind of abrupt change due to some systemic break then I don’t think the alternative will be a positive outcome for humanity (since it will likely be a centrally plan solution being force-fed to us as the solution).

I do, however, not think that the solution to the problem will come from within the system that created the problem in the first place. Humans are not good at solving big problems until we are forced to. This is why we have been kicking the can down the road for the past few decades (by creating more and more debt). If a better solution arises that works better than what we have today, however, we will quickly adopt it (remember the iPhone). I believe Bitcoin (the asset and the protocol) has properties that make it superior to the existing solutions we have in a lot of ways (a faster, cheaper, more open monetary system and a harder, more scarce money). When new technologies arrive, and they are superior in every way to the existing technologies they win. If people begin to agree that Bitcoin is better monetary technology, then it will continue to grow and will help us solve our problems.

I don’t know the answer to which one is better (Keynesian or Austrian) or which one wins in the long run (or if either does). I don’t think either will in my lifetime. I think that less central control and a more free market are better. I have a hunch that basing our money (something that is at the core of everything on this earth) on something that cannot be printed out of thin air by anyone at any time is a better option. So, I sympathize with the Austrians greatly. But these are extremely complex topics and I’m just a poor boy from a small town in Tennessee. I could be wrong and if I am I don’t want to get wiped out. So, how do I proceed?

My Take

I have chosen my warrior for the final boss battle, and it is Bitcoin. I believe it is a viable solution to everything that is written here. I have continued to move more and more of my wealth into that system over time. I will continue to do so as time passes. I have not moved everything to this new, burgeoning system just yet, however.

Hence the reason I’m a 60/40 guy (but not like the 60/40 most people know about).

- 60% of my portfolio is financial instruments that are based on the current fiat monetary system (mainly stock ownership). These companies invest capital to produce something that allows them to earn a return.

- 40% of my portfolio is grounded in things that have scarcity and cannot be produced without expending labor/energy (commodities and Bitcoin).

- I do not invest in cash because it is not an investment (and these days it earns next to nothing).

- I do not invest in bonds because the yields will not allow me to outpace inflation AND because they are fiat-derivative contracts. I have used them to park money in the past to ‘have some safety’ but that went away in 2020 for me. I believe they are Certificates of Confiscation that are programmed to debase. How ‘safe’ did you feel in bonds this year when they were down 21% from their peak and inflation was running 7%+ in consecutive years? I’ll take my chances with the wild swings of whatever market I’m invested in.

- I own other real-world things that also cannot be created from thin air and have some scarcity to them (business, residence, land, antique vehicles, etc.). I believe these will keep pace with inflation at the least and provide some diversification as well. Some are even fun to own.

I am ‘uncomfortably long’ risk assets. I’d rather not have to weather the highs and lows of the wild gyrations that Mr. Market presents me to earn a return that enables me to beat inflation in a monetary system that is built on absolute insanity. But as I’ve described that is not possible. So, I will stay the course and stay fully invested in risk assets. Uncomfortably, very, very uncomfortably.

There is a huge caveat here, however. HUGE! I must not be forced to sell until I decide it is time to sell. I can’t run into a liquidity crunch and need to sell assets at a point when I might not want to sell them (i.e. if they are on a wild swing down). I likely want to be adding to my positions during these times (maybe). This is all easier said than done. It is important to have income coming in (or a cash cushion) that you live on, low debt so your existing cash flows are not strained, and low (or no) leverage that could force liquidation if/when asset prices take a hit. Using leverage is tempting since the manipulated money is borderline free. But it comes at a cost if things go wrong and you have problems servicing the debt. So, if you are using leverage, it better be sparing, and non-callable, and your ability to service the debt needs to be high.

My most important asset and allocation, however, is to Bitcoin. It is the apex asset and apex money. The price volatility does not bother me because the price is not the thing I am trying to solve for. I’m running a whole different kind of calculus to solve this global monetary problem. I’m trying to solve the problem of a monetary system that is built on fairy dust that could vaporize my entire life’s wealth at any time. I don’t trust the system or the people running the system to take care of me. With Bitcoin, I can store my wealth and take care of myself without anyone else involved except myself and the decentralized Bitcoin protocol. This part of my wealth is completely outside of the system that I believe is completely broken. I can go anywhere on earth with it inside my brain and trade it for anything and anyone willing to accept it. As the world becomes more and more volatile due to our money being broken, I believe this might be important for me to have. Bitcoin, for me, is not about price but about optionality. I believe more and more people will come to see the value that I see in Bitcoin as time goes on. More do each day. As that happens Bitcoin will demonetize the world. I happen to think this will be a net benefit for every human on the planet. Bitcoin Fixes This! Freedom Money! Fix The Money, Fix The World!

“But Deano, Bitcoin is volatile! Aren’t you down like 80%?!?” – Everyone

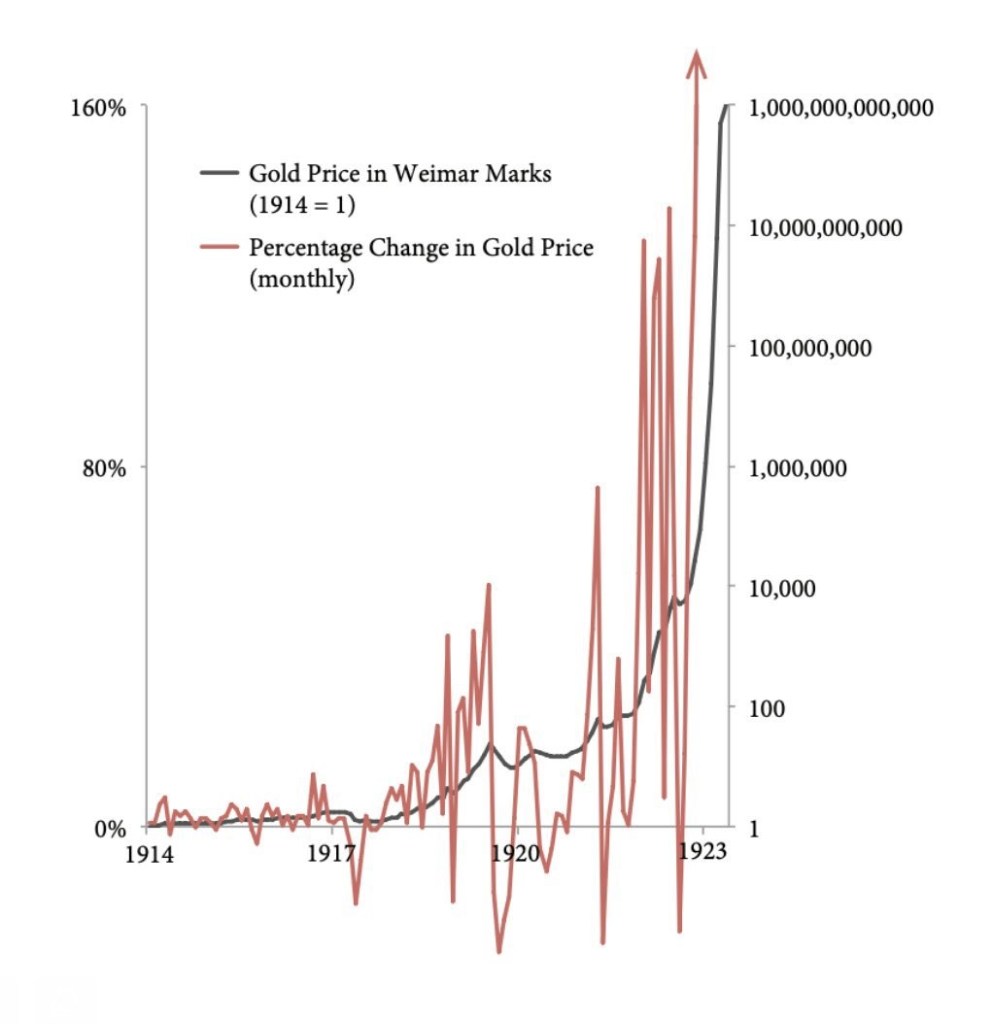

The above chart is ingrained into my mind! Yes, Bitcoin is volatile and if you expect to own it and not be in for a wild ride you are mistaken. I’d point to two things that address this volatility. First, when a monetary system is having problems, the assets being priced in that system’s currency are going to be whipsawed. The above chart shows the price volatility of gold during the Weimar hyperinflation. Despite the extreme volatility, you can see that gold held its purchasing power over time (it went up and to the right). I believe we will see similar price action in Bitcoin (and other monetized risk assets) in our future. Second, Bitcoin is an emerging asset class that many believe won’t even make it (and I guess it might not). Few people know what Bitcoin is, or how it works, fewer own it, and fewer use it. It is a new and nascent technology and like any asset with those properties the value of it will rise and fall a lot and often. Bitcoin, however, has been operating as designed for over a decade, it has been growing for over a decade, and it has done so without fail. If it continues and adoption increases (increasing the network effect of the asset) then it will be volatile but also will increase in monetary value (again, up and to the right). I expect Bitcoin to continue to gain adoption. Regardless, I fully expect volatility and am prepared to hold all risk assets (including Bitcoin) through whatever comes.

Good or bad, if I had to pick only one asset to own for the rest of my life it would be Bitcoin. Regardless, I believe you need to be diversified and don’t believe your own bullshit! I shitpost all kinds of wild stuff on Twitter regularly. I take time on a semi-regular basis to write down my thoughts and share them. This has led to pushback from people at times which has helped me to clarify a position or belief I might hold. This is valuable to me (which is why I write this and share it). It is more for me than anyone who might read it. I have definite thoughts on my view of the financial world. But I don’t go all in on any of it. Because I might be a great big dumbass! Highly likely! That is investing in a nutshell. Don’t let your own opinions or thoughts get in the way of keeping and growing your wealth. No sense in being a damn fool about it!

Conclusion

This is how I go about trying to navigate this messed-up world we find ourselves in. I wish I was smart enough to come up with all of this. I listen to a lot of smart people on the Twitterverse that have helped me figure things out over the years. People like (in no particular order) Preston Pysh, Lyn Alden, Luke Gromen, Jeff Booth, Michael Saylor, Robert Breedlove, Dylan LeClair, Alex Gladstein, Greg Foss, Lawrence Lepard, James Lavish, Ray Dalio, Saifedean Ammous, Jack Mallers, Jason Lowery, Jack Dorsey, Guy Swann, Gigi “DerGigi”, Natali.e.Brunell, Jesse Myers “Croesus”, Luke Broyles, Balaji Srinivasan, Cory Klippsten, Marty Bent, American HODL, Max Keiser, Jeff Snider, Matt Odell, Plan B, and Dominic Frisby.

I’ve listened to many others along the way but these voices stand out in the wisdom they’ve provided and have stood the test of time as events play out. Anyone reading this who knows of them might see the influence of their work. Anyone reading this who doesn’t know who these people are I’d suggest you seek them out. I continue to learn more every day (from them and others).

“Don’t tell me what you think, tell me what you have in your portfolio.” – Taleb (a douche)

I keep track of my investment portfolio and write about my thoughts on investing regularly. Some of the important things I’ve written that outline the things I’ve detailed here as it was happening and I believe have stood the test of time are:

- Twitter Shitposting – I shitpost and fire off other random thoughts as I have them on “the Twitter”: https://twitter.com/deanoroll5

- Being Uncomfortably Long Risk Assets – You can see a major shift in my thinking in 2020. When I saw the response to COVID I immediately exited all bond/cash positions (blue bars). I call this being ‘uncomfortably long’. I explain this here: https://deanorolls.com/2020/12/01/im-uncomfortably-long-assets/

- Why I Own Bitcoin – I own Bitcoin and have written about it twice. The first time was when I bought it in December 2019 here: https://deanorolls.com/2019/12/27/bitcoin-btc/. I did a follow-up in March of 2021 here: https://deanorolls.com/2021/03/09/bitcoin-do-i-still-want-to-own-it/. If you are new to Bitcoin (or want to learn about it start with the second document). Then buy some with me. I’m going to own it forever. HODL!

- Latest Investment Review – I’ve written about my investing journey a good deal. I generally post my positions, allocations, and performance on my website. My most recent update from year end is here: https://deanorolls.com/2023/01/09/2022-investment-review/

- 4-Year Investing Update – I did an exhaustive deep dive on my investment thesis and how I invest my portfolio in late 2021 here: https://deanorolls.com/2021/10/31/4-years-of-being-a-super-nerd-about-investing/

- Why Inflation Is Stupid – I wrote about it twice during 2022 here: https://deanorolls.com/2022/05/05/why-do-we-need-inflation/ and https://deanorolls.com/2022/06/23/is-hyperinflation-coming-preston-pysh/

- Why I Don’t Own Other Crypto – I’ve kept up with other cryptocurrencies (besides Bitcoin) along the way. I never pulled the trigger on buying any of them. I wrote this in November 2021 to outline why here: https://deanorolls.com/2021/11/17/do-i-want-to-invest-in-other-crypto-assets-besides-bitcoin/.

All that said I feel like I’ve got about as good a plan as one can have at this point. I figure I’d share it in case you might find it helpful in your journey. I’d love to know your thoughts on these issues if they are different from mine or the same.

I hope you found something beneficial here. Good luck with your investing and wealth management.

Joey “Deano” Dean

President and Founding Member of Deanco Investment Group (A Very Important Organization)